The Great Uncoupling

The most expensive breakup in corporate history.

The most expensive week in AI history played out like a divorce settlement, a sovereignty dispute, and an earnings call all at once. OpenAI broke up with Microsoft’s exclusivity, moved in with Amazon, and somehow convinced both to keep paying. Beijing retroactively vetoed a deal where the staff had already been hired and the investors already paid out. The EU spent twelve hours arguing about what its own rules mean and then went home. And Big Tech collectively decided that roughly $700 billion in infrastructure spending is a reasonable annual budget for a technology whose revenue model is still, charitably, evolving.

Meanwhile, 78,000 tech workers lost their jobs in Q1, nearly half explicitly because of AI. The machines are getting more capable. The humans are getting angrier. And the checks keep getting bigger.

Free Agent

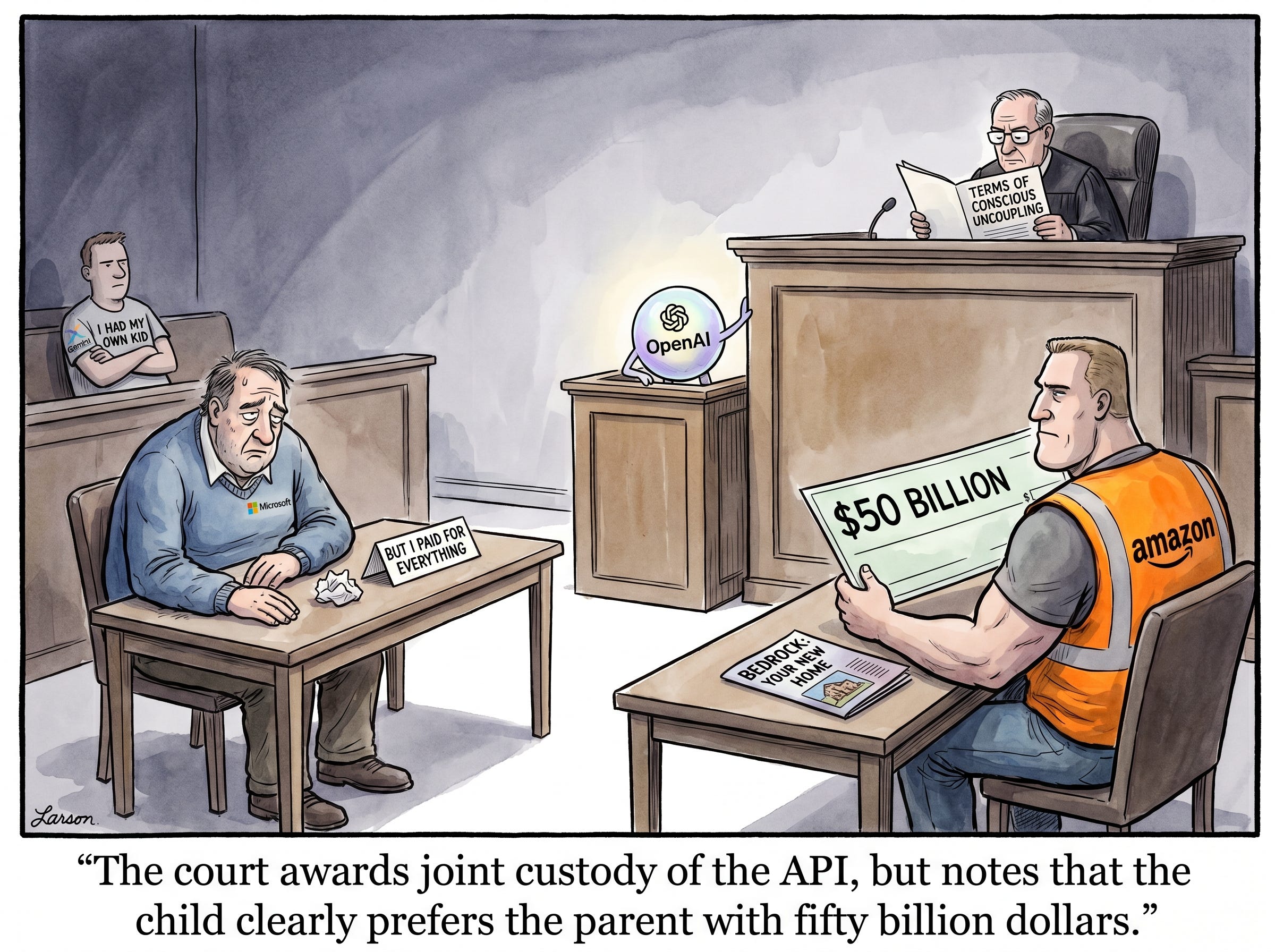

OpenAI and Microsoft announced the end of their exclusivity arrangement on April 27, dismantling the seven-year deal that defined both companies. OpenAI can now serve on any cloud provider. Microsoft’s license to OpenAI technology becomes non-exclusive through 2032. Microsoft no longer pays revenue share to OpenAI, though OpenAI’s payments to Microsoft continue through 2030, subject to a total cap. The restructuring was triggered by Amazon’s $50 billion investment in OpenAI and an exclusive third-party distribution deal for OpenAI’s Frontier platform on AWS.

This is the AI industry’s conscious uncoupling. Sam Altman spent years building on Microsoft’s infrastructure and capital, then leveraged the resulting position to renegotiate the most consequential deal in tech. Microsoft framed it as partnership evolution. Translation: they lost exclusivity, kept the bill, and called it progress. The balance of power has shifted from cloud providers to model builders, and OpenAI just proved that the lab with the leading models can rewrite the terms whenever a richer suitor comes along. The real question is what Azure customers are paying a premium for now that they can get the same models on Bedrock.

CNBC reports on the revenue cap details: OpenAI’s payments to Microsoft are capped, meaning Microsoft’s upside is now fixed while OpenAI’s optionality is infinite. Bloomberg’s financial analysis (paywalled) of the restructuring notes the asymmetry runs even deeper than the headline suggests.

The Veto Heard ‘Round the Valley

China’s NDRC blocked Meta’s $2-3 billion acquisition of Manus on April 27 in a terse one-line notice. This is the same deal I covered in January under “Manus Ex Machina,” when Zuckerberg closed it in ten days and the newsletter noted the “total amputation from China.” Beijing apparently disagrees about who performs the amputation. Manus staff are already integrated at Meta offices. Investors including Tencent, ZhenFund, and Hongshan have already received proceeds. TechCrunch reports the probe ran for months. The unwinding will take longer.

AI M&A now requires sovereign approval from governments that can retroactively disassemble completed transactions. When Beijing can force a company to un-acquire an asset whose employees already have new badges, every cross-border deal in AI carries a risk that didn’t exist two years ago. The technology export control era has arrived, and it looks less like regulation and more like geopolitical repo.

Al Jazeera frames the block as part of Beijing’s broader tech sovereignty play. Fortune’s analysis focuses on the investor fallout: when proceeds have already been distributed, who gives the money back?

The GDP of Switzerland

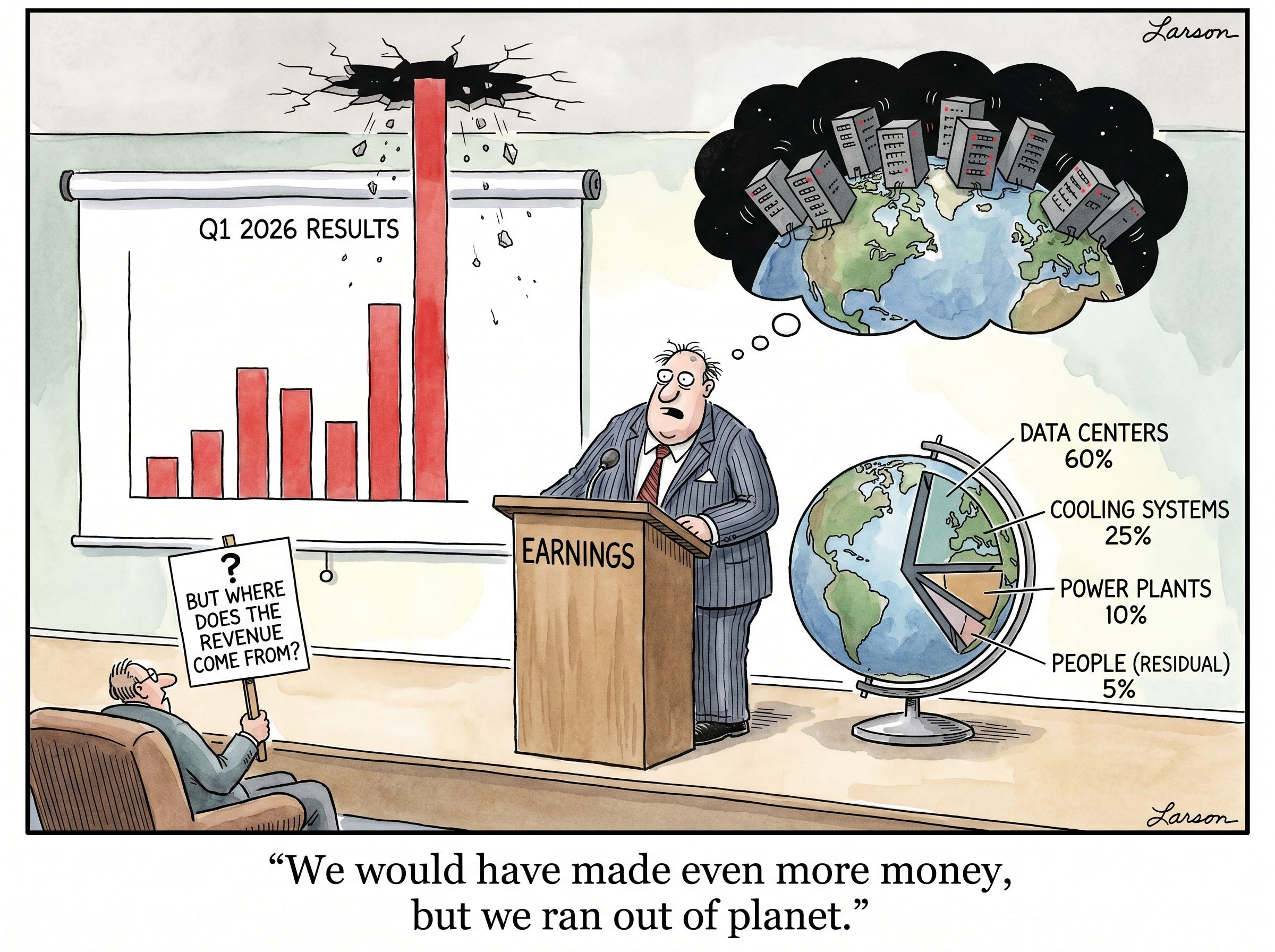

Alphabet, Microsoft, Amazon, and Meta reported earnings April 29, with Apple following today. Combined AI infrastructure spending for 2026 now exceeds $700 billion after Meta raised its capex guidance to $125-145 billion. Microsoft reported $190 billion capex with an EPS of $4.27 (beat), Azure revenue up 40%. Google Cloud hit $20 billion revenue with 63% year-over-year growth, and Alphabet raised capex guidance to $180-190 billion. Amazon committed approximately $200 billion.

Every major tech company on earth is now spending more on AI infrastructure than most countries spend on defense. The results beat Street forecasts, which is the financial equivalent of “the surgery was successful but the patient is still bleeding.” Fortune’s combined capex analysis reveals that whether this is visionary investment or collective mania depends entirely on whether AI revenue catches up to AI spending before someone blinks. Azure at 40% growth outpacing AWS suggests Microsoft is winning the cloud AI race despite losing OpenAI exclusivity. Or maybe because of it. When you lose the exclusive date, you try harder at dinner.

The Next Web’s combined analysis notes that every hyperscaler is now compute-constrained, meaning revenue would have been even higher if they could build data centers faster. The ceiling isn’t demand. It’s physics, and public sentiment.

Seventy-Eight Thousand Canaries

78,557 tech workers were laid off in Q1 2026, with 47.9% directly attributed to AI and workflow automation. Over 150,000 tech jobs eliminated across 500+ companies since January. CNBC reported that Meta and Microsoft jointly announced 20,000+ cuts in April. Block cut headcount nearly in half, from 10,000 to under 6,000, explicitly citing AI. A new academic study warns of a self-defeating “automation trap” where excessive automation erodes the consumer demand that AI products need.

The AI job displacement crisis has gone from theoretical to measurable. Nearly 80,000 tech workers lost their jobs in one quarter, and half those losses are directly linked to AI. Fortune published a first-person account from a worker whose role was eliminated by the same technology they were told to adopt. When the companies building AI are also the ones firing the most people because of AI, the industry’s workforce promises start to sound less like commitments and more like marketing copy.

Twelve Hours in Strasbourg

The European Commission, Council, and Parliament walked out of a 12-hour trilogue session on April 28, failing to agree on a planned postponement of the August 2, 2026 high-risk AI compliance deadline. The impasse centers on conformity assessment for AI in regulated products, specifically how the AI Act intersects with the Machinery Regulation, MDR, and IVDR. The August deadline now stands unchanged. A follow-up trilogue is expected around May 13.

Companies face an immovable compliance deadline while the legislators who wrote the rules still argue about what they mean. The Next Web covered the collapse and its implications: regulatory uncertainty is now at maximum, which is the worst possible state for companies trying to plan compliance investments. The EU wants to control AI but can’t agree fast enough to keep pace with deployment. Twelve hours of debate, zero resolution, and a deadline that keeps getting closer. The clock in Brussels runs on a different timezone than the one in San Francisco, and the gap is widening.

Fifty States, Zero Agreement

The White House released its National AI Policy Framework with legislative recommendations for Congress, pushing preemption of “unduly burdensome” state AI laws. Congress has repeatedly rejected federal preemption in both the One Big Beautiful Bill Act and NDAA. States continue advancing their own frameworks: Colorado’s AI Act and California’s CCPA amendments are moving forward regardless.

The White House wants to preempt state AI laws but Congress keeps saying no, and the result is regulatory chaos where neither federal nor state rules have clear authority. Fifty states writing their own AI rules while the federal government debates preemption creates a compliance nightmare for any company operating nationally. No new federal rulemaking body means existing agencies (FTC, SEC) will interpret AI through frameworks designed for different technologies. The US regulatory approach to AI is currently: nobody’s in charge, everybody has opinions, and the only thing both parties agree on is that they can’t agree on anything.

Ballot Measures

Anthropic published election safeguards for the 2026 midterms on April 24, achieving neutrality scores of 95-96% across Claude models. For the first time, they tested whether AI models can carry out influence operations autonomously, and with safeguards in place, models refused nearly every task. Sonnet 4.6 and Opus 4.7 responded appropriately 90% and 94% of the time.

The first AI lab to publicly test and publish results on whether its models can be weaponized for election interference. The transparency is notable and the methodology is published for anyone to replicate, which is more than any competitor has offered. But the 90-94% appropriate response rate means 6-10% of influence operation attempts get through. At scale, that’s significant. Publishing the vulnerability alongside the defense is either radical transparency or a sophisticated trust-building and PR exercise. (Almost certainly both.)

Anthropic’s transparency cum PR push extends beyond elections: Project Glasswing (covered in “Scar Tissue”) continues expanding its coalition of defenders using Claude Mythos Preview to find zero-day vulnerabilities before attackers do.

Long Tail

The Biggest Seed in History

London-based Ineffable Intelligence, founded by AlphaGo co-creator David Silver, raised $1.1 billion in seed funding at a $5.1 billion valuation. Led by Sequoia and Lightspeed, with participation from Nvidia, Google, Index Ventures, and the UK Sovereign AI Fund. The largest seed round in history went to a company nobody outside AI research has heard of, thanks to the mind power (for now) of its humans.

Humanoid Robots for the Last Mile

Shanghai-based Robot Era raised over $200 million for humanoid robotics, led by logistics giant SF Express. A logistics company leading the round signals commercial deployment, not R&D demos. China’s humanoid robotics race is accelerating while the West debates whether humanoid form factors are even the right approach. SF Express isn’t debating.

The Plumber’s AI Agent

Avoca raised $125 million from Kleiner Perkins for AI agents that handle front-office operations for HVAC, plumbing, and roofing businesses. Founded after a chance encounter at a Texas home services event. When plumbers and roofers use AI to answer phones, the technology has crossed from knowledge work into the trades. Blue-collar AI is the market most of Silicon Valley forgot existed.

Prophet Margins

Q1 2026 shattered records: $300 billion in global VC funding. AI accounts for 3 of every 5 deals in April (764 of 1,314 tracked). The money isn’t flowing. It’s flooding.

Amazon invested $5 billion in Anthropic with up to $20 billion more in future rounds, building on its previous $8 billion.

Anthropic expanded its partnership with Google and Broadcom for multiple gigawatts of next-generation compute infrastructure. Anthropic is now the most multi-cloud AI lab, taking money from everyone simultaneously.

Rogo raised $160 million Series D for agentic AI in investment banking, led by Kleiner Perkins. Total funding above $300 million. Bankers replacing bankers with AI funded by bankers.

Aidoc raised $150 million Series E for hospital diagnosis AI. Nine-figure vertical AI rounds are becoming routine, which is either a sign of maturation or a sign of peak.

Eclipse closed a $1.3 billion fund targeting physical AI, manufacturing, and defense applications. The atoms economy wants its AI moment.

OpenAI acquired Hiro Finance, its seventh known acquisition in 2026. The approximately 10-person team joined OpenAI, with Hiro shutting down by April 20. The acqui-hire cadence is now monthly.

NEC and Anthropic announced a collaboration to build Japan’s largest AI engineering workforce. The talent shortage is global, and solving it requires partnerships that look more like nation-building than recruiting.

Google DeepMind released Gemma 4 in four sizes under fully permissive Apache 2.0, the first Gemma models with no commercial restrictions. The 31B model ranks #3 on Arena AI. Open source keeps getting more competitive.

Slop of the Week

The MAGA Cheat Code

A 22-year-old Indian medical student used Google’s Gemini to create a fake pro-Trump influencer named “Emily Hart,” a blonde nurse in MAGA caps and flag bikinis. Gemini literally suggested a “MAGA woman” as a “cheat code” because “the conservative audience (especially older men in the U.S.) often has higher disposable income and is more loyal.” Reels pulled 3-10 million views before the account was banned and documented by the OECD. When the AI provides the blueprint for its own exploitation, the product has become the con.

Are You Hallucinating?

Who Let The Dogs Out?

Robot dogs with silicone heads modeled on Elon Musk, Jeff Bezos, Mark Zuckerberg, Andy Warhol, and Pablo Picasso are roaming Berlin’s Neue Nationalgalerie. Beeple’s “Regular Animals” features each robot photographing visitors and “processing” images through AI filters mimicking its namesake’s style, then ejecting printed art in a gesture mimicking digestion. The Picasso dog makes cubist images. The Warhol dog makes pop art. The Bezos dog probably optimizes for Prime delivery speed. The Washington Post confirmed the art they excrete is for sale.

Your attention is a precious, non-renewable resource. Thanks for spending some of it here.

I read every reply and it means a lot, so if you have feedback or something to share, please do. Don’t be a stranger. Humanity is all we have left.